Inside Norway’s $2.1 Trillion Wealth Machine & the Macro Playbook for the Next 10 Years

A Strange New World — And How to Profit as an Investor

“There are no certainties about the future only probabilities.”

— Unknown

Not financial, investment, legal, or tax advice. Please read our full Disclaimer on the Disclaimer page. Accessible via the provided link and via the homepage menu. Continued reading constitutes your agreement to its terms.

The Norwegian Government Pension Fund Global (GPFG), or “Oil Fund,” is the world’s largest sovereign wealth fund, with over US$2.1 trillion in assets as of December 2025. About US$1.5 trillion are in global equity investments. The rest is in fixed income, real estate, and infrastructure.

Norway did well economically but wasn’t a wealthy country until massive oil reserves were discovered in the 1960s. After building out the oil industry, in 1990, Norway decided to establish a sovereign wealth fund (a fancy term for the country’s investment fund), called the Norwegian Government Pension Fund Global (GPFG).

It is massively successful. So successful that I want to repeat something: this fund is now the world’s largest sovereign wealth fund. That is no small accomplishment for a country of roughly 5.6 million people. To put that in perspective, the Washington, D.C., metro area has a population of about 5.6 million.

So, for every man, woman, and child in Norway, the GPFG holds about US$375,000 in assets.

To put that in perspective, a family of four would theoretically have ~$1.5 million in the fund on their behalf. This is one of the highest sovereign wealth fund per capita ratios in the world.

The Fringe Finance Report covered this wealth fund first in February 2025. If you want to read more about the background of this wealth fund, we covered it in the original article, which you can read here.

This fund publishes its list of global investments twice a year, sometime during Q1 and sometime during Q3. For us investors, that’s a rare treat. We get to see in detail where this truly global investor—with extremely smart people—invests worldwide. That angle—worldwide—was always interesting, but it has become extra interesting in this changing world of ours. This world of ours is changing so rapidly with so many moving variables that it can be tempting to assume the future looks like the past. But nothing could be further from the truth. In Chapters 1 through 4, we provide an organized approach on how to structure one’s thoughts about the future—given the many, many moving variables.

We’ll get to what the fund actually owns in Chapter 5. First, we need to understand the world it’s investing into.

Having said that, let’s jump into that strange new world of ours—and see how we can profit from it as investors.

Chapter 1: The New Macro Reality — The Known Knowns

Norway’s Government Pension Fund Global isn’t just a big investment account. It’s a promise. Built from the country’s oil wealth, its job is to turn a resource that will eventually run out into a permanent source of wealth for future generations. With over $2 trillion, it owns a small piece of nearly every major public company on Earth. Its time horizon isn’t measured in quarters or even decades—it’s measured in generations.

But even the most patient investor has to ask: What kind of world are we investing in?

As of early 2026, the answer is complicated. For about forty years, investors operated in a relatively stable environment: interest rates generally fell, global trade expanded, and U.S. leadership provided a kind of anchor. That era is ending. What’s replacing it is more complex, more volatile, and far less predictable.

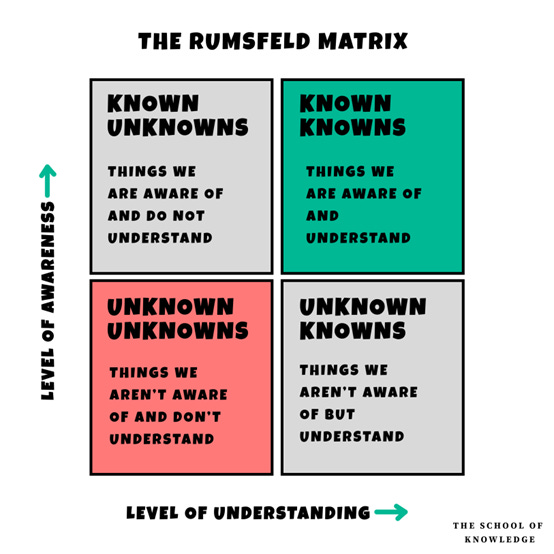

So how do we think clearly about uncertainty? One useful framework comes from an unexpected source: a 2002 press briefing by then-U.S. Secretary of Defense Donald Rumsfeld. When asked about evidence linking Iraq to weapons of mass destruction, he offered a simple but powerful way to categorize knowledge:

“There are known knowns. There are things we know we know. We also know there are known unknowns; that is to say, we know there are some things we do not know. But there are also unknown unknowns—the ones we don’t know we don’t know.”

— U.S. Secretary of Defense Donald Rumsfeld 2002

Later thinkers added a fourth category: unknown knowns— Things we understand (know) on some level but ignore or dismiss. These are often blind spots—such as dismissing a risk because “it hasn’t happened to us yet.”

I know, at first, it makes your head hurt. What is this?

But stay with me. This is a really good thought model once you let it sink in.

Image source: https://www.theschoolofknowledge.net/p/the-rumsfeld-matrix-explained

Let’s walk through each category as it applies to the global investment landscape.

A word of caution: the future is never certain. There are only probabilities, not certainties. But some probabilities are so high that we treat them as certain—the known knowns.

Chapter 1.1: Known Knowns: The Structural Certainties

These aren’t guarantees. But there’s strong evidence behind them, enough that a long-term investor can build a strategy around them. In simple terms, if you could jump 10 years into the future, this is where we’d most likely end up. This section is less about how we get there and more about where we finish.

Fiscal dominance in the United States is a known known.

Macroeconomic analyst Lyn Alden defines fiscal dominance as a situation where a government’s debt and deficits become so large that the central bank can no longer set interest rates solely to control inflation. Instead, it must keep rates low enough to ensure the government can service its debt.

The U.S. federal debt now exceeds $39 trillion. Annual deficits run above $2 trillion even during economic expansions. Interest payments on the debt now surpass the entire defense budget.

Here’s how “melting the debt” works: inflation helps reduce the burden of debt without actually paying it off. As prices and wages go up, the economy grows in dollar terms—that’s GDP. Even if total debt keeps rising, it becomes smaller compared to the size of the economy (GDP), if the economy keeps growing faster. The key number is debt as a percentage of GDP. If that percentage goes down, the debt becomes more manageable—not because it was paid off, but because the economy grew bigger around it. Everything gets more expensive. But given the size of the debt and political realities, we have no other choice. And we are already on that path.

The Fringe Finance Report covered Lyn Alden’s fiscal dominance theory back in July 2025, in the article called “How Smart Investors Get Rich From Inflation (While Everyone Else Suffers)” in Chapter 2 “Fiscal Dominance – We Lost Control.”

The dollar’s reserve currency status provides a buffer.

Even with big deficits and rising debt, the U.S. dollar has a unique advantage: it is the world’s main reserve currency. It means global demand for dollars stays strong. Central banks hold dollars. Trade is priced in dollars. Investors buy U.S. assets for safety. It’s being eroded mainly by our actions—we’ll get into that more below—but for now, it’s still holding strong – although on a slow, long-term decline as reserve currency. It is still going very strong as a trading currency.

This demand lowers borrowing costs for the U.S. government. This doesn’t mean the dollar can’t lose value over time. It does mean the decline is likely to be gradual, not sudden. A trend, not a cliff.

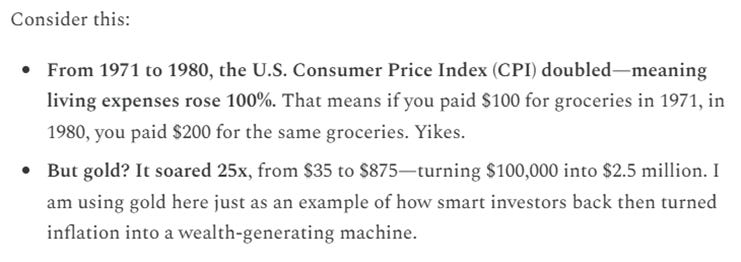

The long-term erosion of the dollar’s purchasing power is a known known.

Legendary gold and silver investor Rick Rule draws a direct parallel to the 1970s, when U.S. inflation erased a lot of the dollar’s purchasing power over a single decade. He expects history to rhyme, with the dollar losing about 75% of its purchasing power over the next ten years—not through a sudden crash, but through persistent inflation that steadily outpaces official targets.

What changes is what a dollar can actually buy: a barrel of oil, a month of rent, or groceries. In a nutshell, everything becomes more expensive, so the same $100 buys less and less. The dollar will likely still do well versus other major Western currencies like the EU, UK, or Japan, as they face similar issues. But like those currencies, the same dollar amount will still buy you less over time.

Here is what we said in the above-mentioned article:

Source: https://ffus.substack.com/p/how-smart-investors-get-rich-from

AI adoption is a known known.

Here’s what we know: AI will change how we work, produce, and compete over the next 10, 20, and 30 years. More about this further below.

Global demographic trends are a known known.

Across most developed nations, birth rates have fallen below the replacement level of about 2.1 children per woman. It is 2.1 because 2 children are needed to replace the parents once they die to keep the population the same, and the 0.1 is to make up for early deaths like accidents. In South Korea, for example, the birth rate is a horrible 0.8. I wish I could say South Korea is a bad example, but unfortunately not. Populations are aging. Workforces are shrinking. Pension and healthcare systems face rising pressure. This isn’t a short-term cycle. It’s a structural shift. Fewer workers supporting more retirees means slower economic growth, higher taxes or deficits, and more competition for labor.

For investors, this favors companies that can raise prices, automate tasks, or serve aging populations. It also adds to inflationary pressure over time, as labor becomes scarcer and wages rise. Maybe AI can help offset that inflationary trend. But the low birthrate is a global problem for the developed world. However, Africa has currently the highest birth rate in the world at 4.1 while everyone else is hovering around 2.1 or lower (most are lower).

The shift to a multipolar world is a known known.

For decades after the Cold War, the world operated under a single dominant power: the United States. That order supported a global system built for efficiency: just-in-time supply chains, open trade routes, and clear rules.

That era is ending. We are moving into a multipolar world, where the U.S., China, Russia, the EU, India, and others compete for influence and resources. Each is trying to secure access to critical materials like chips, energy, minerals, and rare earth elements.

Rare earths are a perfect example. These 17 metals or so are essential for smartphones, electric vehicles, and fighter jets. For years, China controlled most of the mining and processing. Now, other countries are racing to build their own supply chains—not because it’s cheaper, but because relying on a single source is too risky.

Energy security follows the same logic. The conflict in the Middle East (Iran war) has reminded the world that oil supplies can be cut off without warning. That has renewed interest in uranium. Uranium packs an enormous amount of energy into a small space. A single fuel pellet holds as much energy as a ton of coal. A warehouse full of uranium can power a city for decades. After Fukushima in 2011, many countries stepped back from nuclear power. But when the choice is between no electricity—or accepting the risks of modern nuclear technology—the math changes.

The result is higher costs for everyone. Just-in-time gives way to just-in-case. For a long-term investor, this means the old playbook—globalization equals lower costs—no longer applies universally.

We covered the shift to a multi-polar world in August 2025 in an article called “A Strange New World – And How To Make Money From It.”

Elevated geopolitical tension is a structural feature.

As the famous Prussian war strategist Carl von Clausewitz wrote, “War is politics by other means.” In a multipolar world, competition between major powers doesn’t disappear—it shifts form. Economic pressure, cyber operations, proxy conflicts, and military posturing become tools of statecraft.

Recent conflicts in Ukraine and the Middle East are not isolated events. They are symptoms of a broader realignment. Potential flashpoints—Taiwan, the South China Sea, the Arctic, Eastern Europe—carry similar risks. For investors, this means political risk is no longer a side note. It is central to asset allocation, security selection, and risk management. That means for the time being, many countries will spend more on their military.

We just talked about the known knowns — things about the future that are so likely we can treat them as certain. The path to that future may be smooth or rough, but the outcome is almost guaranteed.

In the next chapter, we move on to the known unknowns — things we know will happen at some point in the next 10 years, maybe more than once, but we do not know exactly when.

Chapter 2: The Uncertain Path — The Known Unknowns

These are things we know we cannot predict. In investing, they aren’t reasons for paralysis—they’re invitations to prepare for a range of outcomes. Allow me to be morbid for a second. A known known is that we will all die—eventually. A known unknown is the question of when and how. Hopefully of old age, far, far in the future—but we don’t know. That is a known unknown.

Are we overdue for a recession or stock market crash?

The S&P 500 has been in a bull market for more than a decade. Historically, that length of time without a major downturn is unusual. Many investors feel we are “due” for a correction. Legendary investors seem to agree. Jim Rogers has long warned of a major market reset. Warren Buffett’s Berkshire Hathaway has held record levels of cash—over $300 billion in early 2026—waiting for better opportunities. Even aggressive investors like Rick Rule, who typically favors hard assets, has noted the value of holding dry powder when valuations look stretched.

If history holds, a stock market crash and/or recession should happen at some point. When? We don’t know. From a pure valuation perspective, though, the U.S. stock market looks very expensive.

But here’s the twist: in an age of fiscal dominance, maybe the old rules don’t apply. If governments and central banks are committed to keeping markets stable to protect their own borrowing costs, maybe downturns are shallower, shorter, or delayed. The Turkish stock market offers a cautionary example: as the lira lost value, local stocks rose in nominal terms. Investors who held equities preserved purchasing power—even as the currency fell.

So is this time different? Maybe. But “this time is different” are four of the most dangerous words in investing. History doesn’t repeat, but it often rhymes. The safe approach isn’t to bet everything on a new paradigm. It’s to prepare for both possibilities: a continued melt-up driven by liquidity, or a sharp correction when sentiment shifts.

Rick Rule recently increased his cash holdings significantly. This isn’t his preference, but he believes there is now more than a 20% chance of a stock market crash exceeding 50%. He notes that holding cash is expensive: Treasury bills pay just under 4%, while he estimates real inflation, not CPI inflation, at around 8%. That means each year he holds cash, he loses about 4% in purchasing power. If a market crash happens, the move will pay off. If not, the cost will be the lost purchasing power.

The timing and path of the dollar’s decline is a known unknown.

That the dollar will lose purchasing power over a decade is a known known. But will it happen smoothly? Or in sudden jumps? A crisis could speed things up. Or it could be so slow you barely notice until you look back. We can’t time this. So we prepare for both.

The path of AI adoption—and who wins—is a known unknown.

That AI will transform the economy is a known known. But we don’t know how we get there, which companies will lead, or which business models will survive. The dot-com boom is a guide. The internet did transform the economy—just not how most expected in 1999. Many hyped companies failed. A few quiet winners changed everything.

Adding uncertainty: AI is now a national security issue. In a multipolar world, the U.S., China, and others will pour money into AI—regardless of short-term returns. This speeds development but adds political risk. Regulations, export controls, and tech decoupling could reshape the landscape overnight.

For investors: AI is too important to ignore. But concentration is risky. The destination is clear. The journey is not.

US Treasury OFAC sanctions risk in a multipolar world is a known unknown.

In a world of competing powers, economic tools like sanctions are used more often—and with less warning. For U.S. investors, this creates a specific risk: even foreign stocks traded on U.S. exchanges can be forced to be sold, or frozen with no clear end date. The Office of Foreign Assets Control (OFAC) makes these decisions based on foreign policy goals—not the financial impact on U.S. investors.

When elephants fight, the grass gets trampled. U.S. investors holding foreign assets—even when purchased through their U.S. broker at U.S. stock exchanges—can be caught in the crossfire. Good luck getting your money back.

Real-world examples:

In 2021, China Mobile was delisted from U.S. stock exchanges due to executive orders. Investors had to sell, often at a loss.

In 2022, Russian stocks trading on U.S. stock exchanges were frozen due to an executive order. No trading. No exit. No timeline for resolution to this date (4 years later).

In neither case did U.S. investors travel to China or Russia to buy local securities. Their “mistake” was believing that foreign securities approved by the SEC and purchased through U.S. brokers on U.S. exchanges couldn’t simply be outlawed overnight by presidential order—without compensation. However, that is the reality.

We know this risk exists. We don’t know when it will strike next, or which holdings will be affected. That uncertainty demands diversification, careful jurisdictional analysis, and humility about what we can control.

Geopolitical conflicts and policy responses are known unknowns.

We know the Strait of Hormuz faces disruption. We know energy prices can spike. We know governments will intervene in crises. We know it will likely be bad, but don’t know how bad, as we don’t know how it will resolve. Next week? A bigger war that will keep the Strait closed until next year? Or even longer? No one knows. The vulnerability isn’t just oil — it’s the boring stuff we never think about - until it breaks: the global supply machine. And this won’t be the last conflict in the next 10 years.

What is important to note is that many of these conflicts can be seen as proxy wars with other large powers in this multipolar world of ours. Ukraine is a proxy war with Russia. Iran is a proxy war with BRICS, as Iran is a member. Taiwan is a proxy war with China. Note that we have few, if any, wars that don’t involve the other emerging large powers. Sadly, during times of global power shifts, that is more normal than not.

Now we know what will likely happen (the known knowns) – the destination. We know that the path to that destination will depend on things that will likely happen, but we don’t know when (the known unknowns). Let’s take a look at the assumptions we stopped questioning—the unknown knowns. Our blind spots. And let’s also look at the unknown unknowns—the black swan events—like COVID.

Chapter 3: Blind Spots, Black Swans, and Preparing for the Future

Chapter 3.1: Unknown Knowns: Things we understand (know) on some level but ignore or dismiss.

“U.S. Treasuries are always safe in a crisis.” Maybe not anymore.

For decades, investors fled to U.S. Treasury bonds in times of stress. But in a world of fiscal dominance—where the sovereign borrower is also a source of instability—this assumption may no longer hold. Early signs: when Middle East tensions rose in 2026, 10-year Treasury yields went up, not down. If bonds stop being a safe haven, many portfolio strategies would need rethinking.

And the 2022 sanctions on Russia changed the game globally. When the U.S. froze Russian central bank assets—including U.S. Treasury holdings—it sent a clear message: if Treasuries can be frozen when held by Russia—the world’s largest country and a nuclear superpower—then any country is potentially at risk. This wasn’t a panic. It was a quiet but sustained shift. Central banks from China to allies like Poland have been steadily increasing their gold holdings ever since. Not a run for the exit, but a continuous repositioning toward assets that can’t be frozen by a foreign government.

“Global diversification protects me.” Maybe less than we think.

Norway’s fund owns 7,200+ companies across 60 countries. Diversification looks at correlation numbers. However, what is often overlooked is that correlation is a living, breathing thing. During calm times, assets that seem uncorrelated may in a crisis become very correlated all of a sudden. During the 2007-2008 financial meltdown, stocks, bonds, commodities, and emerging markets fell all at once. Correlation isn’t a fixed number in a spreadsheet. It changes with fear, liquidity, and policy. It is alive.

“The U.S. security umbrella guarantees the system — the dollar, the trade routes, the rules.”

For decades, the unspoken assumption was that American hard power stood behind the global financial order. The U.S. Navy kept sea lanes open, the U.S. military enforced red lines, and the dollar’s reserve status drew strength from the belief that the U.S. could — and would — defend the system against catastrophic disruption. That assumption meant energy flowed, trade contracts were honored, and foreign central banks could accumulate dollar reserves without questioning the physical security of the assets behind them.

It is no longer safe to assume this. The 2022 freeze of Russian central bank reserves — including U.S. Treasuries — demonstrated that financial assets held in the U.S. system could be weaponized overnight, even against a nuclear superpower. It was a precision strike aimed at Moscow. It became a slow-acting poison for the dollar’s credibility, as central banks from Beijing to Warsaw quietly shifted reserves into gold, an asset no foreign government can freeze. Then the Iran conflict drove the point home physically. Drones and cheap anti-ship missiles revealed that the U.S. Navy — still formidable — is touchable in certain scenarios. Forward bases in the Middle East proved vulnerable. The Strait of Hormuz, the world’s most critical energy chokepoint, could not be reliably kept open.

The message to allies and adversaries alike was unmistakable: the guarantor of last resort cannot always guarantee. When hard power is perceived as finite (still powerful, but not all powerful any longer), the premium embedded in dollar assets — the assumption of unshakable stability — begins to erode. Not in a single crash. Nothing dramatic. But steadily, and structurally, slowly over time. As an American, this is not something I want, but as equity investors we need to operate in the world that is, not the world that we want it to be.

“This time is different for tech valuations.” Are we sure?

Today’s tech leaders are profitable and cash-rich—unlike the dot-com era. But market concentration now exceeds 2000 bubble levels. Believing “this time is different” is exactly the kind of assumption the unknown knowns category warns us to question.

Chapter 3.2: Unknown Unknowns: The Unforeseeable (The Black Swan)

By definition, these are events we cannot anticipate: a pandemic from an unexpected source, a technological breakthrough that upends industries, a geopolitical shift that redraws alliances.

The 2020 COVID-19 pandemic is a perfect example. No major model predicted a global shutdown starting from a wet market in Wuhan. Yet within months, borders closed, supply chains broke, and central banks unleashed unprecedented stimulus. Markets plunged, then roared back. Entire industries—travel, offices, retail—were reshaped overnight. That’s an unknown unknown: not just surprising, but transformative.

The only responsible posture is humility and a margin of safety. A portfolio that is robust across a wide range of known scenarios is more likely to survive the unknown ones.

What we can observe: unknown unknowns cluster around periods of rapid change. The current moment—shifting alliances, record debt, AI revolution, fragmented trade—is precisely when surprises are most likely. Thinking in decades, not quarters, isn’t a luxury. It’s essential.

Chapter 3.3: A Probability Space, Not a Prediction

The Rumsfeld framework separates four categories of knowledge: what we know will happen in the long term (known knowns), what will happen but we don’t know when or how (known unknowns), “facts” that are no longer true (unknown knowns), and black swan events like COVID (unknown unknowns).

So why use a probability space at all? Why not just pick the most likely outcome and go all-in? Because the future doesn’t work that way. Because no one can predict the future. The best we can do is to think what the potential future could be and create a portfolio that will do well in all scenarios.

Below are four future scenarios: Default Base Case, Alternative Base Case, Along the Way, and The Surprise Nobody Saw Coming.

Given the above, for the US, the Default Base Case is the likely long-term scenario. But if the Iran war turns ugly and becomes a long war—or if something similar happens in the future—the Alternative Base Case becomes possible. Once resolved (if resolved), we should default back to the Default Base Case.

Then there are two wild card scenarios that, if history is any guide, will happen at some point—though we don’t know when. Recessions, stock market crashes, wars, and events like COVID fall into this bucket. These are: Along the Way: Sudden Drop, Then Quick Bounce (The “Panic & Rescue”) and The Surprise Nobody Saw Coming (The “Curveball”).

1. The Default Base Case: Prices Go Up, But Your Money Buys Less (The “Slow Squeeze”)

What Actually Happens: Governments let inflation run a bit high to make debt easier to handle. Stock prices and asset prices rise in dollar terms, but your paycheck doesn’t stretch as far. Supply chains get more expensive. AI and tech keep growing. The dollar weakens slowly, not suddenly.

What This Means for Stock Investors: Companies that can raise prices (brands, essentials, energy) do better than those that can’t. Gold, commodities, and uranium tend to hold value. Bonds lose real value. Cash loses purchasing power. Own things that can’t be printed.

2. The Alternative Base Case: High Prices + Slow Growth (The “Stuck Economy”)

What Actually Happens: Energy prices stay high due to conflict or supply issues. Inflation stays elevated. Economic growth is weak. Central banks are stuck: raise rates and hurt growth, or cut rates and fuel inflation. AI investment continues, but profits get squeezed.

What This Means for Stock Investors: Energy, commodities, and uranium stocks may outperform. Companies with strong pricing power survive. Active management and flexibility matter more.

3. Along the Way: Sudden Drop, Then Quick Bounce (The “Panic & Rescue”)

What Actually Happens: A shock hits—a war flare-up, a bank problem, a geopolitical surprise. Markets drop fast. Everything falls together, even gold. Central banks and governments step in with support. Markets recover, often led by hard assets.

What This Means for Stock Investors: Keep some cash ready so you’re not forced to sell at the bottom. Gold, miners, and energy stocks often bounce back fastest. Diversification may not protect you during the drop—but it helps during the recovery.

4. The Surprise Nobody Saw Coming (The “Curveball”)

What Actually Happens: Something outside our current thinking happens: a major cyberattack on financial systems, a new pandemic, a sudden tech breakthrough, or an unexpected geopolitical shift.

What This Means for Stock Investors: No model predicts this. The only defense is true diversification (across assets, regions, and strategies) and keeping a margin of safety—cash, optionality, humility.

Chapter 4: Chapters 1 through 3 in A Nutshell – The Next 10 Years

The Next 10 Years in 5 Bullets

1. Fiscal dominance + aging demographics → Persistent inflation. Your cash and bonds slowly leak value.

The U.S. debt is too big to repay honestly. The math is clear: the only politically survivable way out is to let inflation run hot, year after year. Prices rise, wages rise, the economy grows in dollar terms, and the debt shrinks relative to the pie. That’s “melting the debt.” At the same time, the developed world is aging fast. Fewer workers, more retirees. Labor gets scarcer. Wages get pushed up. More inflationary fuel.

2. Multipolar world → Higher costs, less trust in Treasuries. Central banks buy gold.

The old global order ran on efficiency: open borders, just-in-time supply chains, the U.S. as a security umbrella. That era is ending. We’re in a world of great-power competition. Supply chains are rebuilt just-in-case—energy, chips, rare earths. Redundancy costs money.

3. Geopolitical tension → Sudden shocks (energy spikes, market panics) followed by policy rescues (money printing) that feed more inflation.

In a multipolar world, friction isn’t a bug. It’s a feature. Ukraine, the Middle East, Taiwan—not isolated events, but symptoms of a structural realignment. For investors, that means energy and supply shocks are now permanent. A flare-up closes the Strait of Hormuz, oil spikes, markets sell off overnight. Central banks, trapped by high debt, ride to the rescue with liquidity. That feeds the inflation engine again. It’s a loop: shock, panic, rescue, more inflation.

4. AI → A productivity wild card, but trapped inside national security politics. No clear winners yet.

AI will reshape the economy over the next 10, 20, 30 years. That we know. How? We don’t know. It could offset aging demographics and cool inflation with a productivity surge. Or it could cause an AI spending boom and a tech bubble that doesn’t really help the real economy. The extra catch: AI is now a national security priority. Governments pour money into it no matter what the returns are. Like the dot-com revolution of the early 2000s, AI will change a lot, but we don’t know how yet.

5. The bottom line → Own hard assets. Keep dry powder.

Put it all together, and the likeliest destination is the “Slow Squeeze”: asset prices rise in dollar terms, but your purchasing power steadily leaks away. Hard assets—gold, commodities, uranium, companies with pricing power—preserve real wealth. Bonds and cash slowly bleed value. Along the way, there will be panics where even gold gets sold in the scramble for liquidity. That’s when dry powder matters. And hanging over everything are the unknown unknowns—curveballs you can’t predict, only prepare for.

The One Behavioral Trap to Avoid - FOMO

Over the next 10 years, there will be moments when everyone around you is piling into whatever is rallying—tech after a breakthrough, gold during a panic, crypto on hype. The FOMO will be real. The discipline to stick with a humble, robust portfolio—owning tangible assets you understand, keeping a margin of safety—is what separates those who preserve wealth from those who chase and crash. At least if you need to do FOMO, limit the size to amounts you can afford to lose.

Now, let’s see what Norway’s $2.1 trillion fund actually owns.

In the following sections, we will cover the following:

Chapter 5: Inside Norway’s $2.1 Trillion Wealth Machine - Where the Money Actually Goes — The Full Picture

Chapter 6: The Art of Exclusion — Known Unknowns and the Risks the Fund Refuses to Take

Chapter 7: The American Elephant — The Unknown Knowns in the U.S. Concentration

Chapter 8: The Forgotten Corners — Known Unknowns and the Countries the Fund Got Right

Chapter 9: The Investor’s Playbook — What You Can Steal from the World’s Largest Wealth Fund